What is an Assumable Mortgage and How Does Mortgage Assumption Work? If you are exploring…

Self-Employed Borrowers in Southwest Washington: Underwriting Tactics That Turn Variable Income Into Approval

Navigating Mortgage Approvals as a Vancouver Entrepreneur

Securing a mortgage as an entrepreneur or freelancer in Clark County can feel like an uphill battle. Traditional lenders often struggle to understand variable income, leaving many talented business owners scratching their heads. Fortunately, Mortgage and Credit Pro specializes in helping self employed borrowers in Southwest Washington achieve their homeownership dreams.

If you are a tech professional running a startup or a local business owner in Vancouver WA, understanding how underwriters view your income is crucial. Here are some of the primary hurdles self employed buyers face:

- Inconsistent Cash Flow: Monthly income fluctuations can make standard debt to income calculations tricky.

- Tax Deductions: While great for your tax bill, aggressive write offs lower your qualifying income.

- Business Structure Complexity: Sole proprietorships, LLCs, and S Corps all require different documentation.

By working with an experienced Vancouver mortgage broker, you can leverage specialized underwriting tactics to turn these challenges into approvals.

Bank Statement Programs and Income Add Backs

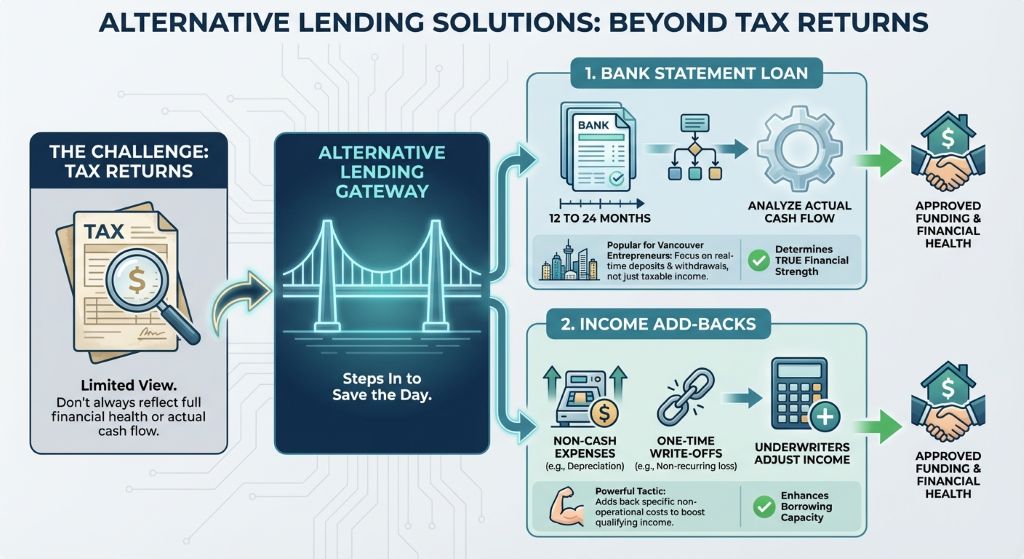

When tax returns do not tell the full story of your financial health, alternative lending solutions step in to save the day. One of the most popular options for Vancouver area entrepreneurs is the Bank Statement Loan. Instead of relying on tax returns, lenders analyze 12 to 24 months of personal or business bank statements to determine your actual cash flow.

Another powerful tactic is utilizing income add backs. Underwriters can add certain non cash expenses or one time write offs back to your bottom line. These commonly include:

- Depreciation on equipment or real estate.

- Amortization of business assets.

- One time casualty losses.

- Business use of home deductions.

Understanding these flexible options allows you to maximize your purchasing power in the competitive Southwest Washington real estate market. Reach out to our local Vancouver office to see which strategy fits your unique business model.

| Loan Program | Income Verification Method | Ideal Borrower Profile | Typical Down Payment |

|---|---|---|---|

| Traditional Conventional | 2 Years Tax Returns | Established businesses with high net taxable income | 3% to 5% |

| 12-Month Bank Statement | 12 Months Business/Personal Deposits | Freelancers and contractors with steady cash flow | 10% to 20% |

| 1099 Only Loan | 1-2 Years of 1099 Forms | Independent contractors and gig economy workers | 10% to 15% |

| DSCR (Investor) | Property Rental Income | Real estate investors looking to expand portfolios | 20% to 25% |

Preparing Your Business for Mortgage Success

Preparation is the key to a smooth underwriting process. John Werner and the team at Mortgage and Credit Pro recommend taking proactive steps at least six months before you plan to buy a home in Southwest Washington. First, keep your personal and business finances strictly separate. Commingling funds is a major red flag for underwriters and can complicate your income calculation.

Next, consult with both your CPA and your mortgage professional before filing your annual taxes. Sometimes, taking fewer deductions in the year you plan to buy can significantly boost your qualifying income. Finally, maintain a healthy credit profile and keep a solid reserve of liquid assets to show lenders you have a safety net.

If you are ready to explore your home loan options, do not let variable income hold you back. With the right underwriting tactics, your entrepreneurial success can translate directly into the keys to your new home.

Q1: How long do I need to be self-employed to qualify for a mortgage in Vancouver, WA?

Most traditional lenders require a two-year history of self-employment. However, if you have transitioned from a W2 role in the same industry, some flexible programs may only require one year of self-employment.

Q2: What is a bank statement mortgage program?

A bank statement program is a non-QM loan that allows self-employed borrowers to qualify based on the average monthly deposits in their personal or business bank accounts, rather than using tax returns.

Q3: Can I use my business funds for a down payment?

Yes, you can use business funds for a down payment, provided you are the primary owner of the business and your CPA can verify that withdrawing the funds will not negatively impact the operations of the company.

Q4: How do income add-backs work for self-employed borrowers?

Underwriters can add non-cash expenses, like depreciation and amortization, back to your net income. This effectively increases your qualifying income and helps lower your debt-to-income ratio.

Q5: Do bank statement loans have higher interest rates?

Because they are considered alternative documentation loans, bank statement programs typically have slightly higher interest rates than conventional loans. However, they offer the flexibility needed to secure an approval without showing high taxable income.

Call John Werner at Mortgage and Credit Pro to Discuss Your Self-Employed Mortgage Options Today!

Related Posts