Why an FHA Loan Might Be Your Best Path to Homeownership Welcome to your comprehensive…

Your Complete Guide to FHA Streamline Refinance in Vancouver WA

Understanding the FHA Streamline Refi Process

If you currently have an FHA loan and are looking to lower your interest rate or reduce your monthly payments, an FHA streamline refinance might be the perfect solution. Also known simply as an FHA streamline, this program is specifically designed to make the refinancing process as smooth and efficient as possible. As a local mortgage broker based in Vancouver, WA, I am here to help you navigate your options and secure the best possible terms.

Unlike a traditional rate and term refinance, an FHA streamline refi requires significantly less paperwork. The Federal Housing Administration allows lenders to use the original paperwork from when you bought the home, which means less hassle for you. Whether you want to drop your mortgage insurance premium or secure a lower interest rate, this program offers a fantastic opportunity for homeowners in Washington, Oregon, and Arizona.

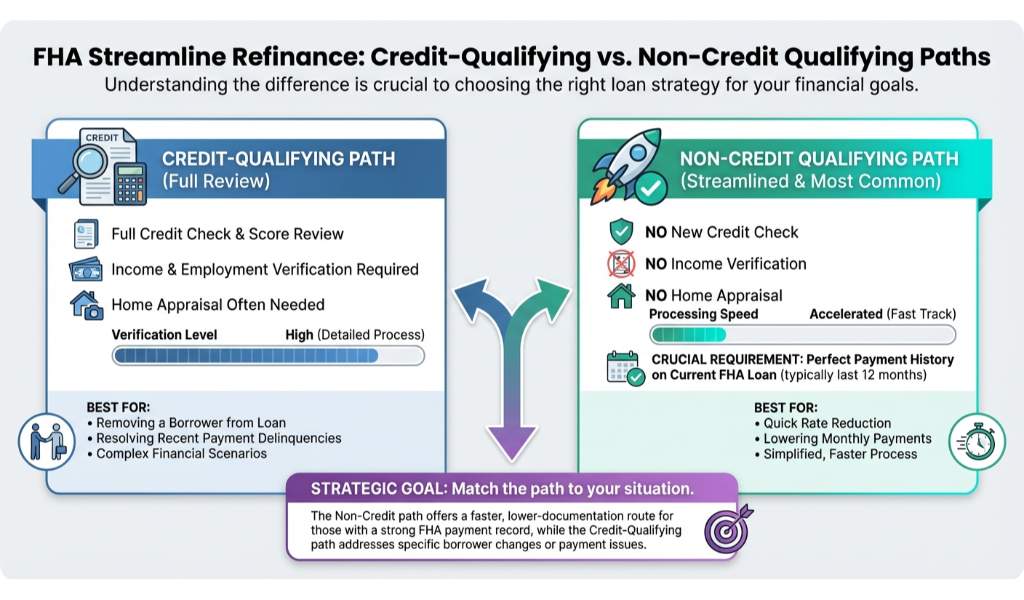

Credit-Qualifying vs Non-Credit Qualifying FHA Streamlines

When exploring an FHA streamline refi, you will encounter two main paths: credit-qualifying and non-credit qualifying. Understanding the difference between credit-qualifying vs non-credit qualifying is crucial to choosing the right loan strategy for your financial goals.

- Non-Credit Qualifying: This is the most common type of FHA streamline. It does not require a new credit check, income verification, or a home appraisal. As long as you have a perfect payment history on your current FHA loan for the last six months, you can generally qualify.

- Credit-Qualifying: This option requires the lender to verify your income and credit score. You might choose a credit-qualifying FHA streamline if you have had a change in borrowers on the mortgage, such as removing a spouse after a divorce, which requires proving the remaining borrower can handle the payments.

We are experts at providing second opinions on FHA streamline refinance applications. If another lender has told you that you do not qualify, or if you simply want to ensure you are getting the most competitive rate, reach out to our team at Mortgage and Credit Pro.

| Feature | Non-Credit Qualifying | Credit-Qualifying |

|---|---|---|

| Credit Check | Not required | Required |

| Income Verification | Not required | Required |

| Home Appraisal | Not required | Not required |

| Best For | Borrowers wanting a fast process with no changes to the mortgage ticket | Borrowers needing to remove a co-borrower from the loan |

Why Choose Mortgage and Credit Pro for Your Refinance?

My name is John Werner, and my goal is to make homeownership and refinancing easy with tailored loan solutions. Licensed in OR, WA, and AZ, I understand the local Vancouver real estate market and the unique needs of homeowners in the Pacific Northwest. You have likely heard the horror stories about how hard it is to qualify and the mounds of paperwork involved in refinancing. I am here to solve all of that for you.

We pride ourselves on excellent communication and accessibility. Whether you are looking for an FHA streamline refinance or you are an eligible veteran exploring a VA interest rate reduction refinance loan IRRRL, we have the expertise to guide you. Getting a second opinion on your FHA streamline refinance can save you thousands of dollars over the life of your loan, and we are always happy to review your current loan estimate.

Q1: What are the basic requirements for an FHA streamline refinance?

To qualify for an FHA streamline refinance, your current mortgage must already be FHA-insured. Additionally, the refinance must result in a net tangible benefit, such as a lower interest rate or reduced monthly payment, and you must have a perfect payment history on the loan for the past six to twelve months.

Q2: Do I need an appraisal for an FHA streamline refi?

No, one of the biggest advantages of both credit-qualifying and non-credit qualifying FHA streamlines is that they typically do not require a new home appraisal. Your original purchase price or previous appraisal value is used.

Q3: Can I get cash out with an FHA streamline?

No, FHA streamline refinances are strictly for rate and term adjustments. If you need to access your home equity, you would need to look into an FHA cash-out refinance instead.

Q4: How long do I have to wait to refinance my current FHA loan?

You must wait at least 210 days from the closing date of your current FHA loan, and you must have made at least six consecutive monthly payments before you are eligible for an FHA streamline refinance.

Q5: Why should I get a second opinion on my FHA refinance?

Different lenders offer varying interest rates and charge different fees. Because we are experts at providing second opinions on FHA streamline refinances, we can review your current offer to ensure you are truly getting the best deal possible without hidden costs.

Related Posts