Understanding Teacher and Public Servant Loans in Vancouver, WA Public servants like educators, law enforcement…

Unlock Your Home’s Value: The Ultimate Guide to a HELOC Home Equity Line of Credit in Goodyear, AZ

Understanding the Basics: What is a HELOC Home Equity Line of Credit?

Welcome to Mortgage and Credit Pro! I am John Werner, your local mortgage expert in Goodyear, AZ, and I am here to help you navigate the exciting world of home equity. If you have been paying down your mortgage or watching your property value rise, you might be sitting on a goldmine. A HELOC home equity line of credit is a powerful financial tool that allows you to borrow against the equity you have built in your home.

Unlike a traditional loan where you receive a lump sum, a HELOC works much like a credit card. You are given a credit limit based on your home’s equity, and you can draw from it as needed. Whether you are planning major home improvements, consolidating debt, or funding a child’s education, a HELOC offers incredible flexibility.

At Mortgage and Credit Pro, we are experts at providing second opinions on HELOCs. If you have already received a quote, let us take a look to ensure you are getting the best possible terms. Sometimes, exploring other options like a cash-out refinance might even be a better fit for your specific financial goals.

Navigating Variable-Rate and Fixed-Rate Draw Periods

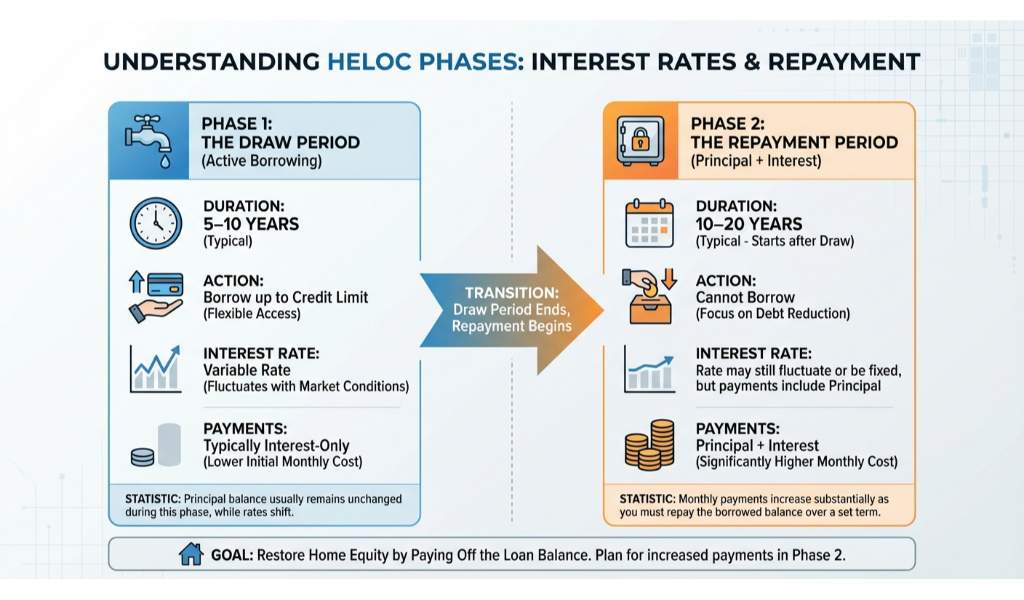

One of the most critical aspects of a HELOC home equity line of credit is understanding how the interest rates and repayment phases work. A standard HELOC is divided into two distinct phases: the draw period and the repayment period.

- The Draw Period: This usually lasts between 5 to 10 years. During this time, you can borrow money up to your credit limit. Most HELOCs feature a variable-rate draw period, meaning your interest rate fluctuates with market conditions. You are typically only required to make interest payments during this phase, keeping your initial monthly costs low.

- Fixed-Rate Draw Periods and Repayment: While variable rates are common, some lenders offer fixed-rate draw periods or the ability to lock in a fixed rate on specific withdrawals. Once the draw period ends, you enter the repayment phase. Your monthly payments will increase because you are now paying back both the principal and the interest. Converting to a fixed-rate repayment plan provides stability and predictable monthly payments.

If you prefer a lump sum with a fixed interest rate from day one, you might want to compare a HELOC to a home equity loan second mortgage. However, for those who want the flexibility to borrow only what they need, the revolving nature of a HELOC is incredibly advantageous.

| Feature | Variable-Rate Draw Period | Fixed-Rate Repayment Period |

|---|---|---|

| Duration | Typically 5 to 10 years | Typically 10 to 20 years |

| Access to Funds | Yes, up to the approved credit limit | No further borrowing allowed |

| Interest Rate | Fluctuates with the market index | Locked in for predictable payments |

| Payment Requirement | Interest-only payments usually required | Principal and interest payments required |

Why Goodyear Homeowners Choose Mortgage and Credit Pro for Their HELOC Needs

Goodyear, AZ is a thriving community, and local property values have seen impressive growth over the years. As a homeowner here, tapping into your equity through a HELOC home equity line of credit can be a smart financial move. However, navigating the fine print of variable-rate draw periods and repayment terms can be overwhelming without the right guidance.

That is where I come in. My name is John Werner, and as a licensed mortgage professional (NMLS #150553), my goal is to make homeownership and financing easy with tailored loan solutions. We pride ourselves on excellent communication and easy accessibility. If you are unsure about a quote you received from another lender, remember that we are experts at providing second opinions on HELOCs. We will review your scenario, explain the pros and cons of variable-rate versus fixed-rate options, and ensure you are positioned for financial success.

Q1: What exactly is a HELOC home equity line of credit?

A HELOC is a revolving line of credit that allows you to borrow against the equity in your home. You can draw funds as needed during the draw period and only pay interest on the amount you actually borrow.

Q2: How does a variable-rate draw period work?

During the draw period, which typically lasts 5 to 10 years, your interest rate can fluctuate based on market conditions. You are usually only required to make interest payments during this time, which keeps your initial payments lower.

Q3: Can I get a fixed rate on my HELOC?

Yes, while the draw period often features a variable rate, many HELOCs allow you to convert some or all of your balance to a fixed rate during the repayment period, giving you predictable monthly payments.

Q4: Do you offer second opinions on HELOCs in Goodyear, AZ?

Absolutely! We are experts at providing second opinions on HELOCs. If you have a quote from another lender, John Werner at Mortgage and Credit Pro will review it to ensure you are getting the absolute best terms possible.

Q5: Is a HELOC better than a cash-out refinance?

It depends heavily on your financial goals. A HELOC is great if you need ongoing access to funds and want to keep your current first mortgage rate. A cash-out refinance might be better if you want a lump sum and a new fixed rate for your entire mortgage balance.

Ready to unlock your home’s equity? Let’s find the perfect solution for your financial goals.

Related Posts