Understanding Condo Loans: Warrantable vs. Non-Warrantable Condos Navigating the world of condo mortgage financing in Goodyear, AZ…

Cash-Out Refinancing in 2026: Unlocking Home Equity for Renovations, Investments, or Debt Consolidation

Is 2026 the Year to Tap Into Your Vancouver Home’s Equity?

As we navigate the housing market in 2026, homeowners in Vancouver, WA, and throughout the Pacific Northwest are sitting on a significant amount of home equity. With property values remaining resilient, a cash-out refinance has become a strategic financial tool for many. Instead of letting that equity sit idle, you can convert it into tax-free cash to achieve major life goals.

At Mortgage and Credit Pro, I hear the horror stories about how hard it is to qualify with big banks—the mounds of paperwork and the endless delays. My goal is to solve that for you. Whether you are in Washington, Oregon, or Arizona, unlocking your home’s potential shouldn’t be a headache. Let’s explore how refinancing this year can help you remodel, invest, or consolidate debt.

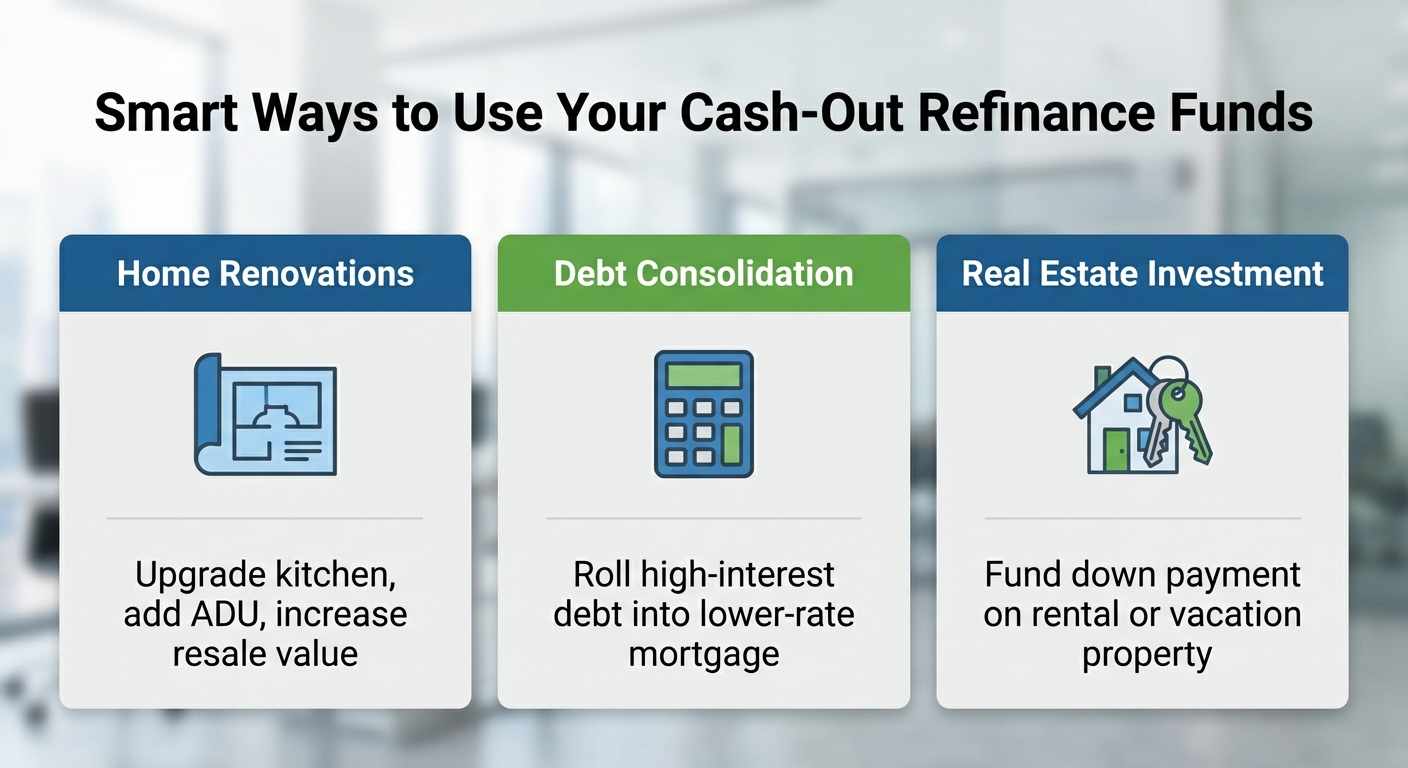

Smart Ways to Use Your Cash-Out Refinance Funds

When you refinance your mortgage and take cash out, you are essentially replacing your current loan with a new one for a higher amount, pocketing the difference. Here are the top three ways our clients are utilizing these funds in 2026:

- Home Renovations: Reinvesting in your property is often the smartest move. Upgrading a kitchen, adding an ADU (Accessory Dwelling Unit), or finishing a basement not only improves your quality of life but can significantly increase your home’s resale value in the competitive Vancouver market.

- Debt Consolidation: With consumer credit card rates often hovering above 20%, rolling high-interest debt into a lower-rate mortgage can save you hundreds, if not thousands, per month.

- Real Estate Investment: Experienced investors often use equity from their primary residence to fund a down payment on a rental property or vacation home, diversifying their portfolio.

| Financial Tool | Average Interest Rate (Est.) | Monthly Cost on $30,000 Debt |

|---|---|---|

| Credit Cards | 22% + | $600+ (Interest Only) |

| Personal Loan | 10% – 15% | $400 – $500 |

| Cash-Out Refinance | Lower Mortgage Rates | Significantly Lower |

Navigating the Process Without the Headache

Many homeowners hesitate to refinance because they dread the process. They fear the fighting, shopping, and haggling typically associated with lenders. As a local Mortgage Broker (NMLS #150553), I pride myself on excellent communication and accessibility. I don’t just work 9-to-5 banking hours; I am here to guide you every step of the way.

To qualify for a cash-out refinance, you generally need to retain at least 20% equity in your home (meaning you can borrow up to 80% of the home’s value). We will review your credit score, current home value, and financial goals to structure a loan that makes sense for you. If you are ready to see if the numbers work in your favor, you can request a quote or view loan scenarios directly on my site.

Q1: How much cash can I take out of my home?

Typically, lenders allow you to borrow up to 80% of your home’s appraised value. The cash amount is the difference between that limit and your current mortgage balance.

Q2: Is the money from a cash-out refinance taxable?

Generally, no. The IRS considers the cash proceeds a loan, not income, so it is usually tax-free. However, always consult a tax professional.

Q3: How long does the cash-out refinance process take?

With a streamlined local broker, the process typically takes 30 to 45 days, depending on how quickly the appraisal can be completed.

Q4: Can I get a cash-out refinance with a lower credit score?

Yes, options like FHA cash-out refinances may allow for lower credit scores compared to conventional loans, though terms may vary.

Q5: Why choose a local broker over a big bank?

Local brokers like Mortgage and Credit Pro offer personalized service, faster closing times, and access to wholesale rates that big banks often cannot match.

Related Posts