Why an FHA Loan Might Be Your Best Path to Homeownership Welcome to your comprehensive…

Your Complete Guide to Condo Mortgage Financing in Vancouver, WA

Understanding Condo Loans: Warrantable vs. Non-Warrantable Condos

Navigating the world of condo mortgage financing in Vancouver, WA can feel overwhelming for first-time buyers and seasoned investors alike. Unlike single-family homes, securing a condo loan involves evaluating both your financial profile and the financial health of the condominium homeowners association (HOA).

At Mortgage and Credit Pro, we specialize in helping buyers understand the complexities of condo loans. The most crucial factor in condo financing is determining whether the property is warrantable or non-warrantable.

- Warrantable Condos: These properties meet the strict guidelines set by Fannie Mae and Freddie Mac. They are typically easier to finance and qualify for standard loan programs, such as a conventional fixed rate mortgage or an FHA purchase loan.

- Non-Warrantable Condos: These complexes do not meet standard agency guidelines, often because a single entity owns too many units, or the project is still under construction. Financing these requires specialized portfolio loans.

If you have been turned down for a condo loan previously, do not lose hope. We are experts at providing second opinions on condo financing and can help you explore alternative options.

Key Requirements for Securing a Condo Mortgage

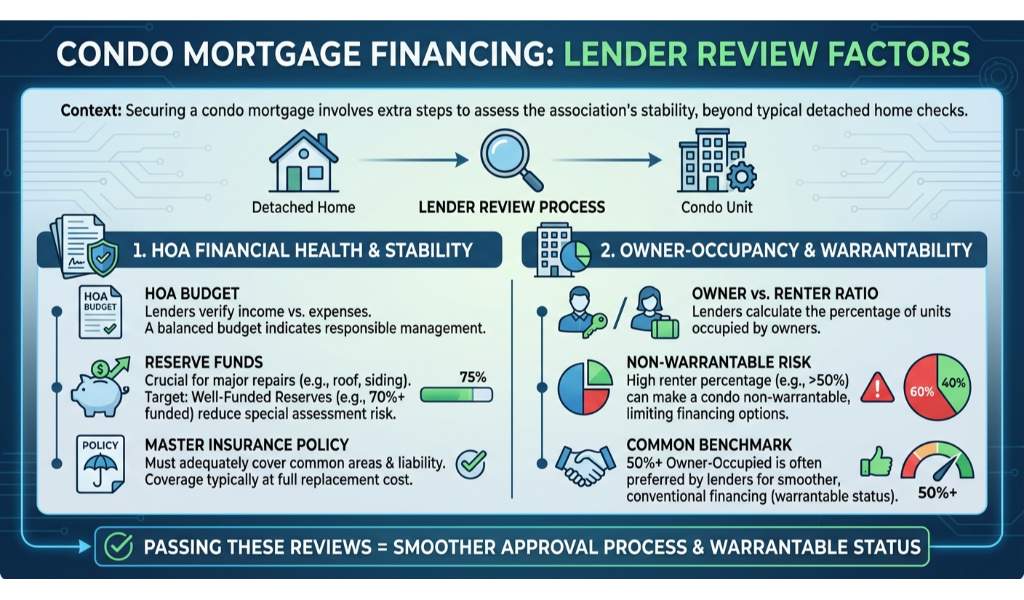

Securing a condo mortgage requires a few extra steps compared to buying a detached home. Lenders need to ensure the condo association is financially stable and adequately insured. Here are the primary factors lenders review during the condo financing process:

- HOA Financial Health: Lenders will request the HOA budget, reserve funds, and master insurance policy.

- Owner-Occupancy Ratios: A high percentage of renters can make a condo non-warrantable, which is especially important if you are seeking an investment property mortgage.

- Litigation: If the HOA is involved in active lawsuits, financing can be temporarily suspended.

Because these guidelines frequently change, working with a local Vancouver mortgage broker like John Werner ensures you have the most up-to-date advice. Whether you are buying a primary residence or expanding your real estate portfolio, understanding these requirements is the key to a smooth closing.

| Feature | Warrantable Condos | Non-Warrantable Condos |

|---|---|---|

| Financing Options | Conventional, FHA, VA | Portfolio loans, specialized lenders |

| Interest Rates | Standard market rates | Typically higher rates |

| Commercial Space | Less than 35% of total square footage | Often exceeds 35% commercial space |

| Entity Ownership | No single entity owns more than 20% | Single entity may own a large percentage |

| Down Payment | As low as 3% to 5% | Usually requires 10% to 20% or more |

Why Get a Second Opinion on Your Condo Loan?

Condo mortgage financing is a highly specialized field. Many big-box lenders automatically deny applications if a condo complex flags as non-warrantable in their system, without exploring alternative solutions. This is where our expertise shines.

We highly recommend getting a second opinion if your condo loan was denied or if you were offered unfavorable terms. At Mortgage and Credit Pro, we have access to a wide network of wholesale lenders and portfolio products that traditional banks simply do not offer. We dig deep into the HOA documents, evaluate the specific reasons for a non-warrantable status, and match you with the right loan product.

Do not let a minor HOA technicality stop you from owning your dream condo in Vancouver, WA. Let John Werner and our dedicated team review your scenario to find a path forward.

Q1: What is condo mortgage financing?

Condo mortgage financing is a specific type of home loan used to purchase a condominium. It requires the lender to approve both the borrower and the condominium project itself.

Q2: What makes a condo warrantable?

A warrantable condo meets the lending requirements of Fannie Mae and Freddie Mac. This typically means the HOA is financially sound, most units are residential, and no single person owns a disproportionate number of units.

Q3: Can I get an FHA loan for a condo in Vancouver, WA?

Yes, you can use an FHA purchase loan for a condo, provided the condominium complex is on the HUD approved condo list or qualifies for a single-unit approval.

Q4: Why are interest rates sometimes higher for condo loans?

Lenders often view condos as slightly higher risk due to the reliance on the HOA for building maintenance and financial stability, which can sometimes result in small pricing adjustments on interest rates.

Q5: What should I do if my condo loan is denied?

Contact us immediately! We are experts at providing second opinions on condo financing and can often find portfolio loan options for non-warrantable condos that other lenders reject.

Ready to secure your condo financing?

Contact John Werner at Mortgage and Credit Pro today for expert guidance or a free second opinion.

Related Posts