Why an FHA Loan Might Be Your Best Path to Homeownership Welcome to your comprehensive…

Your Guide to Securing a First-Time Homebuyer Mortgage in Vancouver, WA

Navigating First-Time Buyer Loans with Confidence

Welcome to the exciting journey of homeownership! If you are looking into a first time homebuyer mortgage, you might feel overwhelmed by the mounds of paperwork and confusing loan terms. At Mortgage and Credit Pro, led by John Werner, we believe buying your first home in Vancouver, WA, should be an exciting milestone, not a stressful ordeal.

Whether you call it a First-Time Home Buyer Mortgage or are simply searching for reliable First-Time Buyer Loans, finding the right financing makes all the difference. We specialize in tailoring loan solutions that fit your unique financial goals. If you already have a quote from another lender, remember that we are experts at providing second opinions on first-time homebuyer mortgages to ensure you are getting the absolute best rate and terms possible.

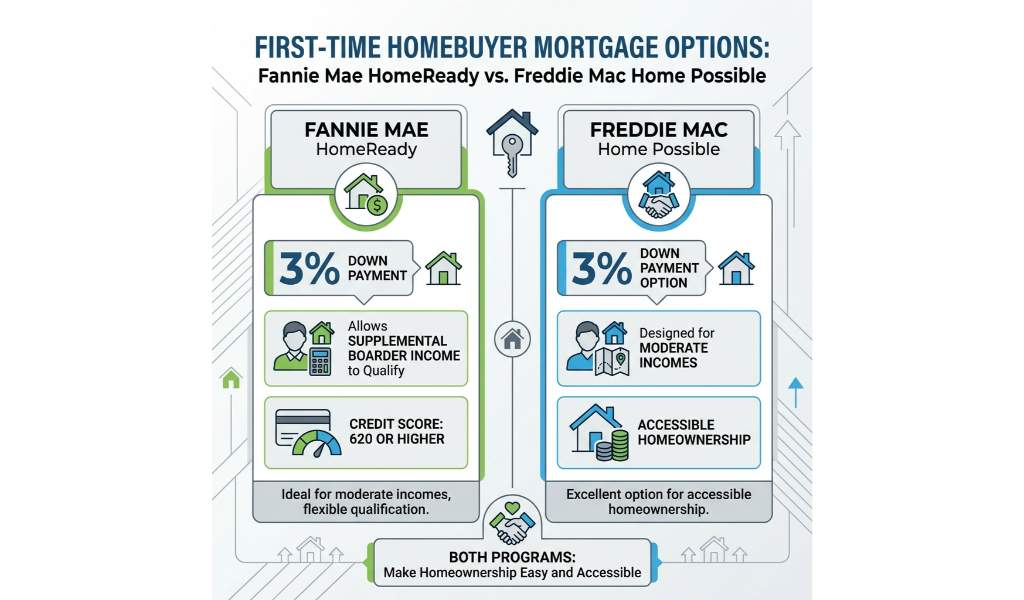

Unlocking HomeReady and Home Possible Loan Programs

Two of the most popular options for a first time homebuyer mortgage are the Fannie Mae HomeReady and Freddie Mac Home Possible programs. Both of these first-time buyer loans are designed to make homeownership easy and accessible, especially for buyers with moderate incomes.

- HomeReady: Requires just a 3% down payment and allows supplemental boarder income to help you qualify. It is an excellent choice if you have a credit score of 620 or higher.

- Home Possible: Also offers a 3% down payment option but is tailored for very low to low-income borrowers. It provides flexible sources for down payments, including gifts and grants.

If you need help with the upfront costs, explore our resources on down payment assistance programs. Alternatively, if your credit score is lower, you might want to look into an FHA purchase loan as a fantastic alternative.

| Feature | HomeReady | Home Possible |

|---|---|---|

| Minimum Down Payment | 3% | 3% |

| Minimum Credit Score | 620 | 620 |

| Income Limits | 80% of Area Median Income (AMI) | 80% of Area Median Income (AMI) |

| Mortgage Insurance | Cancellable once 20% equity is reached | Cancellable once 20% equity is reached |

| Income Flexibility | Allows boarder or roommate income | Allows non-occupant co-borrowers |

Why Get a Second Opinion on Your Mortgage?

You have heard the horror stories about how hard it is to qualify and the fighting, shopping, and haggling to get a good rate. That is exactly why getting a second opinion on your first time homebuyer mortgage is crucial. As a licensed mortgage professional in OR, WA, and AZ (NMLS #150553), John Werner is dedicated to clear communication and easy accessibility.

We review your current loan scenarios and pre-approvals to find hidden fees or better interest rates. A second set of eyes can save you thousands of dollars over the life of your loan. With our expertise, we ensure your first-time home buyer mortgage perfectly aligns with your long-term financial health.

Q1: What qualifies me for a first time homebuyer mortgage?

Generally, you are considered a first-time buyer if you have not owned a principal residence in the past three years. This status opens the door to special first-time buyer loans with lower down payment requirements.

Q2: How much do I need for a down payment?

While traditional loans often require 20 percent, programs like HomeReady and Home Possible allow for just 3 percent down. Other options like VA loans offer zero down for eligible veterans and military members.

Q3: Can I get a second opinion on my mortgage pre-approval?

Absolutely, and we highly encourage it. We are experts at providing second opinions on first-time homebuyer mortgages to guarantee you secure the most favorable terms available in Vancouver, WA.

Q4: What is the difference between HomeReady and an FHA loan?

HomeReady is a conventional loan that requires a minimum credit score of 620 and allows mortgage insurance to be canceled eventually. An FHA purchase loan is government-backed, accepts lower credit scores, but typically requires mortgage insurance for the life of the loan.

Q5: Can I use down payment assistance with a Home Possible loan?

Yes! Home Possible allows you to combine your mortgage with various down payment assistance programs, making it easier to cover your initial costs without draining your savings.

Related Posts