Understanding Condo Loans: Warrantable vs. Non-Warrantable Condos Navigating the world of condo mortgage financing in Goodyear, AZ…

First-Time Homebuyer’s Roadmap for 2026: Overcoming Affordability in Vancouver, WA

Is 2026 Your Year? Navigating the Vancouver Housing Market

If you have been watching the housing market in Vancouver, WA, you know that affordability has been a major hurdle. Between fluctuating interest rates and competitive home prices in Clark County, many aspiring homeowners feel stuck. However, 2026 presents a new landscape of opportunity for those who have a strategic plan.

As a local mortgage professional (NMLS #150553) serving Washington, Oregon, and Arizona, I have heard the horror stories: the mounds of paperwork, the confusion, and the fighting to get a decent rate. My goal is to solve that for you. This roadmap is designed to guide first-time buyers through the complexities of the 2026 market, focusing on smart financing and leveraging assistance programs that big banks often overlook.

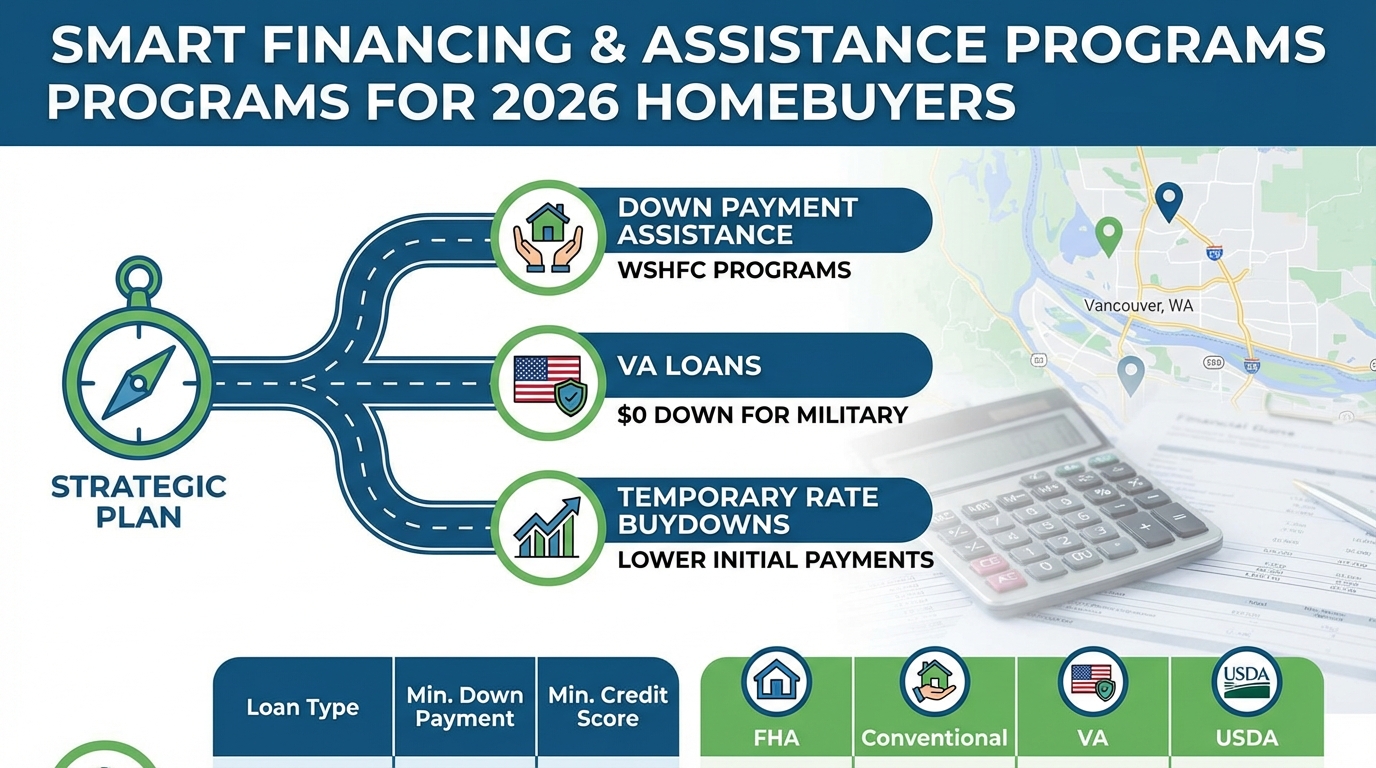

Smart Financing & Assistance Programs You Need to Know

Overcoming affordability challenges isn’t just about finding a cheaper house; it’s about securing a better loan. In 2026, several programs can significantly lower your barrier to entry:

- Washington State Housing Finance Commission (WSHFC) Programs: These can provide down payment assistance to qualified first-time buyers in Vancouver, reducing the cash you need to close.

- VA Loans for Military Families: If you or your spouse have served, you may be eligible for a $0 down VA loan. As a broker who values our veterans, I specialize in navigating these benefits to ensure you get the best terms.

- Temporary Rate Buydowns: This strategy allows sellers to contribute to lowering your interest rate for the first 1-2 years, making monthly payments more manageable while you settle in.

Don’t let the sticker price scare you off before you explore these options. Connect with me to run specific loan scenarios for your budget.

| Loan Type | Min. Down Payment | Min. Credit Score (Est.) | Best For |

|---|---|---|---|

| FHA Loan | 3.5% | 580+ | Buyers with lower credit or smaller savings |

| Conventional | 3% | 620+ | Buyers with good credit looking for lower PMI |

| VA Loan | 0% | None (Lender discretion) | Veterans and active military (Best Terms) |

| USDA Loan | 0% | 640+ | Buyers in designated rural areas of WA |

Why Partner with a Local Vancouver Mortgage Broker?

In a volatile market, who you work with matters. Large retail banks often treat you like a number, leading to the delays and communication breakdowns that kill deals. As a local broker at Mortgage and Credit Pro, I offer a different experience:

- Access to Wholesale Rates: I shop multiple lenders to find you the competitive rate you deserve, rather than forcing you into a single bank’s product.

- Speed and Communication: I pride myself on accessibility. Whether you are making an offer on a weekend or need a quick pre-approval letter for a hot property in Vancouver, I am here to guide you every step of the way.

- Personalized Strategy: From credit repair advice to long-term wealth planning, we look at the big picture.

Q1: What is the minimum credit score needed to buy a house in Vancouver, WA in 2026?

Generally, FHA loans allow for scores as low as 580, while conventional loans typically require 620+. However, I can help analyze your specific credit profile to find the right fit.

Q2: Do I really need a 20% down payment?

No. Most first-time homebuyers put down between 3% and 5%. Programs like VA and USDA loans even offer 0% down payment options for eligible borrowers.

Q3: How do I qualify for down payment assistance in Washington?

Qualification is usually based on income limits and credit score. As a licensed broker in WA, I can screen you for WSHFC programs and other local grants.

Q4: Should I get pre-approved before looking at homes?

Absolutely. A pre-approval letter proves to sellers you are a serious buyer and helps you understand exactly how much home you can afford.

Q5: How is a mortgage broker different from a bank?

A broker partners with multiple wholesale lenders to find you the best rate and product, whereas a bank can only offer their own specific rates.

Related Posts