Why an FHA Loan Might Be Your Best Path to Homeownership Welcome to your comprehensive…

Unlocking Your Home’s Value: A Guide to a HELOC Home Equity Line of Credit in Vancouver, WA

What is a HELOC and How Does It Work?

Welcome to Mortgage and Credit Pro. If you own a home in Vancouver, WA, you might be sitting on a significant amount of untapped wealth. A HELOC home equity line of credit is a highly flexible financial tool that allows you to borrow against the equity you have built in your property over time. Unlike a traditional lump-sum loan, a HELOC functions much like a credit card. You are approved for a specific limit and can draw funds as needed during the initial phase, which is known as the draw period.

During this draw period, you will typically encounter a variable-rate structure where your interest rate fluctuates with the broader financial market. However, many modern lenders now offer fixed-rate draw periods or the option to lock in a portion of your balance at a fixed rate. This provides stability and peace of mind for your monthly budget. If you are weighing your options, you might also want to explore a home equity loan or second mortgage for a one-time lump sum, or consider a cash-out refinance to replace your existing mortgage entirely. We are experts at providing second opinions on HELOCs to ensure you get the absolute best terms possible.

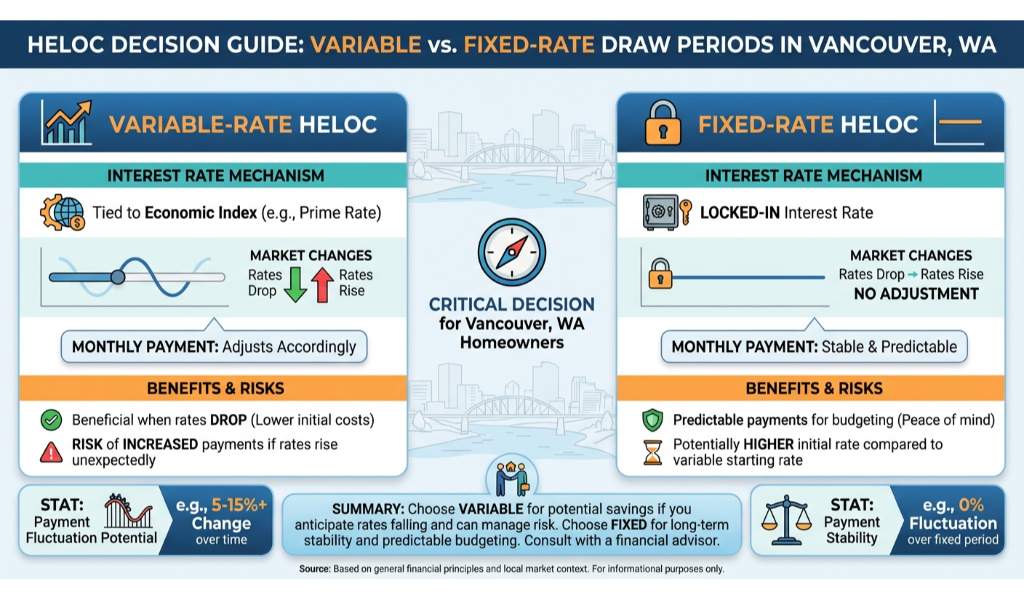

Variable-Rate vs. Fixed-Rate Draw Periods

Choosing between a variable-rate and a fixed-rate HELOC is a critical decision for homeowners in Vancouver, WA. A variable-rate draw period means your interest rate is tied to an economic index, such as the prime rate. As the market changes, your monthly payment will adjust accordingly. This can be highly beneficial when interest rates drop but carries the risk of increasing payments if rates rise unexpectedly.

On the other hand, a fixed-rate draw period allows you to lock in an interest rate for a specific amount of time. This option shields you from market volatility, making it significantly easier to budget your monthly expenses. John Werner, NMLS #150553, and the dedicated team at Mortgage and Credit Pro can help you evaluate your current financial goals to determine which structure aligns best with your needs.

| Feature | Variable-Rate HELOC | Fixed-Rate HELOC |

|---|---|---|

| Interest Rate | Fluctuates with the market index | Locked in for a set period of time |

| Payment Predictability | Low (payments can change monthly) | High (payments remain constant) |

| Best For | Short-term borrowing, falling rate environments | Long-term planning, budget certainty |

| Initial Cost | Typically offers lower starting rates | Slightly higher initial rate in exchange for stability |

Why Get a Second Opinion on Your HELOC?

Navigating the mortgage landscape can be overwhelming. You have likely heard the horror stories about how hard it is to qualify, the endless mounds of paperwork you have to provide, and the haggling required to get a competitive rate. That is exactly why we are experts at providing second opinions on HELOCs. If you have already received a quote from another lender, bring it to us. We will thoroughly review the variable-rate terms, fixed-rate draw periods, and hidden fees to ensure you are truly getting a fair deal.

As a mortgage professional licensed in OR, WA, and AZ, John Werner is dedicated to making homeownership and equity access easy with tailored loan solutions. My clients are the foundation of my success, and I pride myself on excellent communication and easy accessibility when you need me.

Q1: What is a HELOC home equity line of credit?

A HELOC is a revolving line of credit that uses your home as collateral. It allows you to borrow up to a certain limit, pay it back, and borrow again during the designated draw period.

Q2: How long is the typical draw period for a HELOC?

The draw period usually lasts 10 years. During this time, you can access funds and typically only need to make interest payments. After the draw period ends, the repayment period begins.

Q3: Can I switch from a variable rate to a fixed rate?

Yes, many lenders offer a conversion feature that allows you to lock a portion or all of your variable-rate balance into a fixed-rate loan during the draw period.

Q4: How does a HELOC differ from a cash-out refinance?

A cash-out refinance replaces your primary mortgage with a new one at a new interest rate, while a HELOC acts as a separate, secondary loan without altering the terms of your first mortgage.

Q5: Why should I get a second opinion on my HELOC offer in Vancouver, WA?

Lenders offer vastly different rates, fees, and terms. Getting a second opinion from a local mortgage broker ensures you are not overpaying and that the loan structure perfectly fits your long-term financial goals.

Related Posts