What is a Cash-Out Refinance and How Does It Work? If you own a home…

The Ultimate Guide to Adjustable-Rate Mortgages in Vancouver WA

What is an Adjustable-Rate Mortgage (ARM)?

If you are looking to buy a home in Vancouver, WA, you might be wondering if an adjustable rate mortgage is the right choice for your financial goals. An adjustable-rate mortgage, frequently referred to as an ARM, offers an initial fixed interest rate for a specific period before it adjusts periodically based on current market conditions. This is different from a traditional 30-year fixed-rate mortgage or a 15-year fixed-rate mortgage, where the interest rate remains the same for the entire life of the loan.

Many homebuyers choose an adjustable rate mortgage to take advantage of lower initial monthly payments. Here are some of the most common ARM structures:

- 3/1 ARM: Fixed rate for the first three years, adjusting annually thereafter.

- 5/1 ARM and 5/6 ARM: Fixed for five years, then adjusts either annually (5/1) or every six months (5/6).

- 7/1 ARM and 7/6 ARM: Fixed for seven years, followed by yearly or bi-annual adjustments.

- 10/1 ARM: A longer fixed period of ten years before annual adjustments begin.

Whether you are purchasing a new property or looking into a rate-and-term refinance, understanding these terms is crucial.

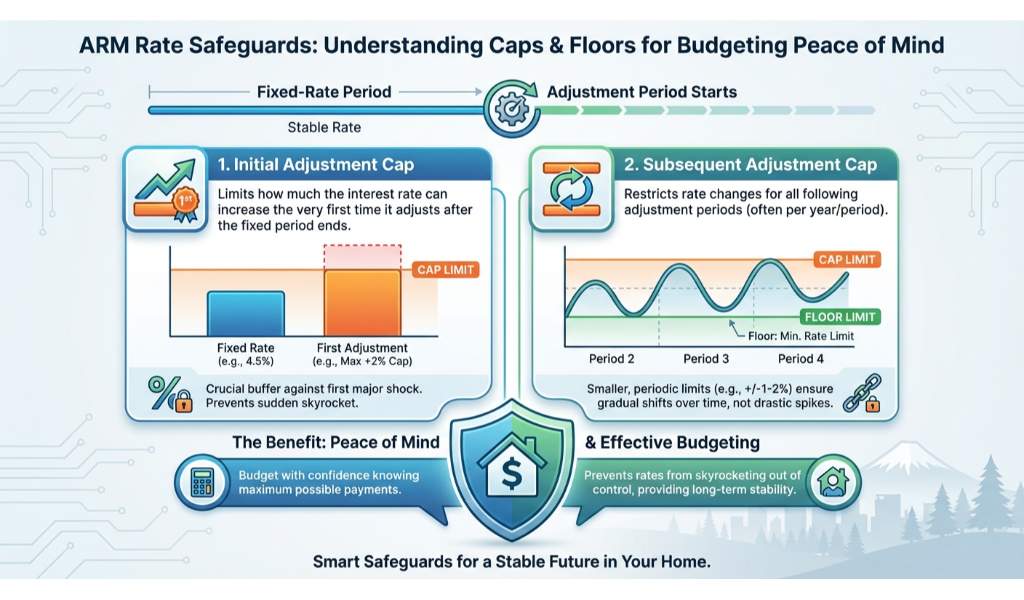

Understanding Caps, Floors, and ARM Adjustments

When considering an adjustable rate mortgage, it is essential to understand how your rate can change. Lenders use specific safeguards known as caps and floors to prevent your interest rate from skyrocketing out of control. These limits provide peace of mind for borrowers in Vancouver, WA, who want to budget effectively.

- Initial Adjustment Cap: This limits how much the interest rate can increase the very first time it adjusts after the fixed period ends.

- Subsequent Adjustment Cap: This restricts the rate increase during each subsequent adjustment period.

- Lifetime Cap: This is the absolute maximum interest rate you will ever pay over the life of the loan.

- Rate Floor: This is the minimum interest rate your loan can drop to, regardless of how low market indexes fall.

These protections are especially valuable if you are financing a high-value property with a jumbo mortgage. At Mortgage and Credit Pro, we highly recommend getting a second opinion on your adjustable-rate mortgage to ensure your caps and floors are truly working in your favor.

| ARM Type | Initial Fixed Period | Adjustment Frequency | Typical Best Use Case |

|---|---|---|---|

| 3/1 ARM | 3 Years | Annually | Short-term homeownership or rapid payoff plans. |

| 5/6 ARM | 5 Years | Every 6 Months | Planning to move or refinance within five years. |

| 7/1 ARM | 7 Years | Annually | Medium-term stability with lower initial rates. |

| 10/1 ARM | 10 Years | Annually | Long-term buyers wanting lower rates than a 30-year fixed. |

Get an Expert Second Opinion on Your Mortgage

Choosing the right home loan is one of the most significant financial decisions you will make. With so many options available, from a 5/1 ARM to a 10/1 ARM, it can be overwhelming to navigate the details alone. That is where John Werner and the team at Mortgage and Credit Pro come in. We specialize in the Vancouver, WA real estate market and pride ourselves on helping clients find the perfect loan structure for their unique needs.

We are experts at providing second opinions on adjustable-rate mortgages. If you already have a quote from another lender, let us review it. We will examine the margins, indexes, caps, and floors to ensure you are getting a competitive and fair deal. Our goal is to empower you with transparent, accurate information so you can buy your dream home with confidence.

Q1: What happens when my adjustable-rate mortgage fixed period ends?

Once the initial fixed period ends, your interest rate will adjust periodically based on a specific financial index plus a margin, subject to your loan caps.

Q2: Is a 5/1 ARM a good idea?

A 5/1 ARM can be an excellent choice if you plan to sell your home or refinance before the five-year fixed period expires, as it typically offers a lower starting rate than fixed-rate loans.

Q3: How often does a 5/6 ARM adjust?

After the initial five-year fixed period, a 5/6 ARM adjusts every six months, rather than annually like a traditional 5/1 ARM.

Q4: Can I refinance an adjustable rate mortgage into a fixed-rate loan?

Yes, many borrowers use a rate-and-term refinance to switch from an ARM to a fixed-rate mortgage before their initial fixed period ends to lock in a stable long-term rate.

Q5: Why should I get a second opinion on my mortgage offer?

Getting a second opinion ensures you are receiving the best possible terms. We review the fine print, including lifetime caps and adjustment margins, to protect your financial interests.

Related Posts