Understanding Condo Loans: Warrantable vs. Non-Warrantable Condos Navigating the world of condo mortgage financing in Vancouver, WA…

The Complete Guide to an Assumable Mortgage in Vancouver, WA

What is an Assumable Mortgage and How Does Mortgage Assumption Work?

If you are exploring the housing market in Vancouver, WA, you might have heard the term assumable mortgage. An assumable mortgage, also known as a mortgage assumption, allows a homebuyer to take over the seller’s existing home loan. This means the buyer assumes the current interest rate, repayment period, and remaining principal balance. In a high-interest rate environment, finding a home with a low-rate mortgage assumption can save you thousands of dollars over the life of the loan.

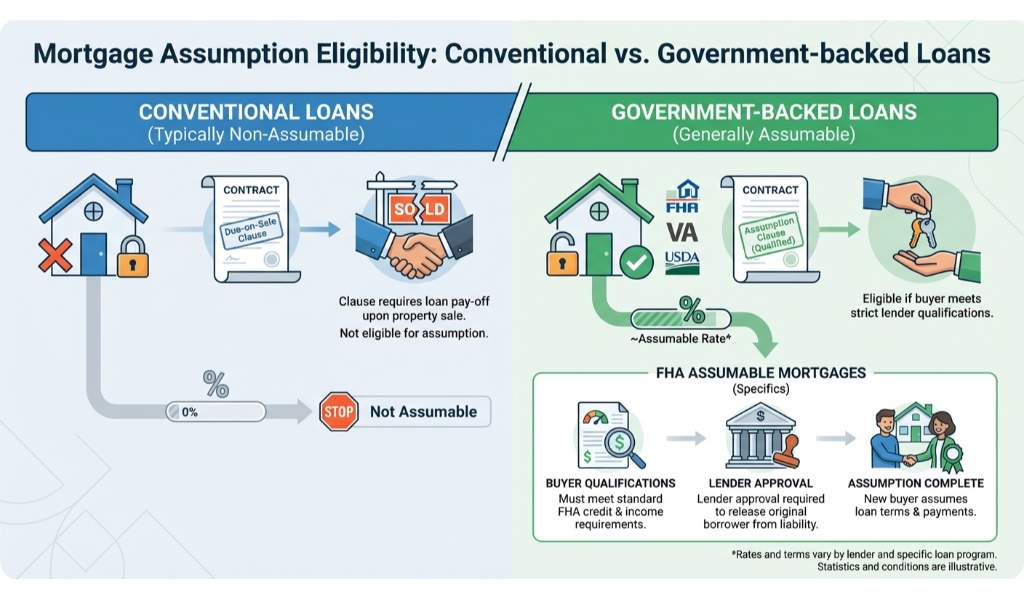

At Mortgage and Credit Pro, we are experts at providing second opinions on assumable mortgages. Whether you are buying or selling, understanding the nuances of these loans is critical. There are three primary types of government-backed loans that typically allow for a mortgage assumption:

- FHA Assumable Loans: Backed by the Federal Housing Administration, these are popular for first-time homebuyers.

- VA Assumable Loans: Guaranteed by the Department of Veterans Affairs, offering excellent benefits for eligible military members.

- USDA Assumable Loans: Designed for rural and suburban homebuyers who meet specific income and location requirements.

While an assumable mortgage is a fantastic option, it is not the only way to secure a great rate. If an assumption is not viable for your unique situation, you might also consider a rate and term refinance down the road to lower your monthly payments.

FHA, VA, and USDA Assumable Mortgages Explained

Not all home loans are eligible for a mortgage assumption. Conventional loans typically contain a due-on-sale clause, meaning the loan must be paid off when the property changes hands. However, government-backed loans are generally assumable, provided the buyer meets the lender’s strict qualifications.

FHA Assumable Mortgages: To assume an FHA loan, the buyer must meet standard FHA credit and income requirements. The lender must approve the mortgage assumption to release the original borrower from liability. If you are interested in starting fresh rather than assuming an existing loan, you can learn more about securing a standard FHA purchase loan.

VA Assumable Mortgages: VA loans are unique because the buyer does not necessarily need to be a military veteran to assume the loan. However, if a non-veteran assumes the loan, the original veteran’s VA entitlement remains tied up in the property until the loan is completely paid off. For veterans looking to use their full entitlement on a new property without complications, applying for a new VA purchase loan might be the better route.

USDA Assumable Mortgages: USDA loans can also be assumed, but typically only with new rates and terms, unless it is a direct family transfer. Standard USDA assumptions require the buyer to meet the strict income and location eligibility guidelines set by the USDA.

Navigating these rules can be complex. That is why Vancouver residents trust John Werner at Mortgage and Credit Pro to provide expert guidance and second opinions on assumable mortgages.

| Loan Type | Assumability Status | Buyer Requirement | Special Condition |

|---|---|---|---|

| FHA Loan | Highly Assumable | Must meet FHA credit and income standards | Requires lender approval for seller release of liability |

| VA Loan | Highly Assumable | Must meet VA credit standards (Veteran status not strictly required) | Seller VA entitlement remains tied to the home if assumed by a non-veteran |

| USDA Loan | Assumable (with restrictions) | Must meet USDA income and property location limits | Often requires new rates and terms unless transferring to a family member |

Why Get a Second Opinion on Your Mortgage Assumption?

A mortgage assumption sounds like a perfect deal, especially when you find a seller with a historically low interest rate. However, there are hidden costs and equity gaps to consider. When you assume an assumable mortgage, you only take over the remaining loan balance. If the home’s purchase price is higher than the loan balance, you must cover the difference in cash or secure a second mortgage to bridge the gap.

Because these transactions involve strict lender approvals and potential equity challenges, getting professional guidance is crucial. We are experts at providing second opinions on assumable mortgages in Vancouver, WA. We will review the seller’s loan terms, evaluate your financial readiness, and help you determine if a mortgage assumption is truly your most cost-effective path to homeownership.

Do not leave your financial future to chance. Let John Werner and the team at Mortgage and Credit Pro analyze your scenario. We ensure you understand every detail of your FHA assumable, VA assumable, or USDA assumable loan options before you sign on the dotted line.

Q1: What is an assumable mortgage?

An assumable mortgage allows a homebuyer to take over the seller’s existing home loan, keeping the original interest rate, repayment schedule, and current loan balance.

Q2: Are all mortgages assumable?

No. Most conventional loans have a due-on-sale clause and cannot be assumed. Government-backed loans like FHA, VA, and USDA loans are typically the only assumable mortgages.

Q3: Do I need to be a veteran to assume a VA loan?

No, non-veterans can assume a VA loan if they meet the lender’s credit requirements. However, the original veteran’s VA entitlement remains tied to the property until the loan is fully repaid.

Q4: How do I cover the equity gap in a mortgage assumption?

If the home price exceeds the remaining assumable mortgage balance, you must pay the difference out-of-pocket with cash or obtain a secondary financing option, depending on lender guidelines.

Q5: Why should I get a second opinion on an assumable mortgage?

The assumption process involves complex lender approvals, potential hidden fees, and equity gap challenges. Getting a second opinion from Mortgage and Credit Pro ensures the deal actually saves you money and fits your long-term financial goals.

Related Posts