Why an FHA Loan Might Be Your Best Path to Homeownership Welcome to your comprehensive…

Boosting Your Credit Score for a Home Loan in Vancouver, WA: Step-by-Step Tips

Buying a home in the Pacific Northwest is a dream for many. Whether you are eyeing a charming craftsman in the heart of Vancouver, WA, a new build in Fisher’s Landing, or a property with acreage in the outer reaches of Clark County, the journey to homeownership begins long before you start touring open houses. It begins with your credit profile.

As a local mortgage professional serving Vancouver and the greater Washington area, I, John Werner, have seen firsthand how a credit score can make or break a real estate transaction. In our current market, where interest rates fluctuate and inventory moves quickly, having a solid credit foundation is your golden ticket to not only qualifying for a loan but securing a rate that keeps your monthly payments affordable.

Many potential homebuyers feel overwhelmed by the concept of “credit repair.” You might have heard horror stories about the difficulty of qualifying or the mounds of paperwork involved. I am here to tell you that with the right strategy, improving your credit score is entirely possible, and it doesn’t have to be a nightmare. At Mortgage and Credit Pro, we specialize in guiding clients through this exact process.

In this comprehensive guide, we will walk through actionable, step-by-Step tips to boost your credit score specifically for mortgage qualification, discuss common pitfalls for Washington residents, and demonstrate exactly how a better score saves you money.

Why Your Credit Score Matters in the Vancouver, WA Housing Market

Vancouver, WA, is a unique market. We are part of the Portland metropolitan area, yet we have our own distinct economic and housing trends. As home prices in Clark County have appreciated, lenders have tightened their standards to ensure borrowers can handle their mortgage obligations.

Your credit score (FICO score) is essentially a numerical representation of your reliability as a borrower. It answers one question for the lender: “If we lend this person money, how likely are they to pay it back on time?”

The Impact on Interest Rates

The most immediate impact of your credit score is on the interest rate you are offered. In the mortgage world, we use “loan-level price adjustments” (LLPAs). These are fees based on risk factors, primarily your credit score and your down payment amount.

- Excellent Credit (760+): You qualify for the best rates available in the market. Lenders compete for your business.

- Good Credit (700-759): You will receive competitive rates, though perhaps slightly higher than the top tier.

- Fair Credit (620-699): You can still qualify for many loan programs (like FHA or Conventional), but you may pay a higher interest rate or require higher mortgage insurance premiums.

- Subpar Credit (Below 620): Qualification becomes more challenging, often restricted to specific government-backed programs like FHA or VA loans, which have more lenient credit requirements but strict debt-to-income ratios.

For residents in Vancouver, WA, where the cost of living is rising, securing a lower interest rate can save you hundreds of dollars a month—money that is better spent on home maintenance, savings, or enjoying the beautiful Pacific Northwest.

The Mortgage Lender’s Perspective: What We Look For

One of the most common frustrations I hear from clients is, “John, my Credit Karma app says my score is 720, but you pulled a 680. Why?”

This is a critical distinction that every homebuyer must understand. Consumer credit apps typically use a scoring model called VantageScore or a generic FICO 8 model tailored for credit cards. However, mortgage lenders use a different set of algorithms entirely.

The “Tri-Merge” Report

When you apply for a home loan, we pull a “Tri-Merge” credit report, which gathers data from the three major bureaus: Experian, TransUnion, and Equifax. We specifically look at:

- FICO Score 2 (Experian)

- FICO Score 4 (TransUnion)

- FICO Score 5 (Equifax)

These older FICO versions are weighted differently than consumer models. They are more sensitive to unpaid collections, high credit card utilization, and recent inquiries. As your lender, I take the middle score of these three. For example, if your scores are 690, 710, and 705, your qualifying score is 705.

Understanding this helps us tailor a strategy to boost the specific factors that mortgage algorithms care about most.

Step-by-Step Tips to Boost Your Score for a Mortgage

If your score isn’t where it needs to be, don’t panic. Credit is fluid. Here are the specific steps I recommend to my clients in Vancouver and throughout Washington to prepare their profiles for a mortgage application.

- Lower Your Credit Utilization Ratio

This is the fastest way to boost a score. Your utilization ratio is the amount of credit you are using compared to your limit. If you have a credit card with a $10,000 limit and a $5,000 balance, you are at 50% utilization.

The Strategy: Aim to get every individual credit card balance below 30% of its limit. For an even bigger boost (the “optimization” zone), get them below 10%. Mortgage FICO scores react very positively when they see you have access to credit but choose not to use it.

- Don’t Close Old Accounts

When you pay off a credit card, your instinct might be to close it to “clean up” your finances. Do not do this.

15% of your credit score is based on the “Length of Credit History.” Closing an old card shortens your average credit age and reduces your total available credit limit, which can spike your utilization ratio. Keep the account open, perhaps putting a small subscription (like Netflix) on it and setting it to auto-pay to keep it active.

- Dispute Inaccuracies

Errors on credit reports are shockingly common. You might have a medical bill from a provider in Vancouver that was paid by insurance but still shows as “unpaid” on your report, or a late payment that was actually made on time.

The Strategy: Obtain your free credit reports from AnnualCreditReport.com. Review them line by line. If you find an error, file a dispute with the specific bureau showing the error. In Washington, consumers have robust protections, and bureaus must investigate disputes usually within 30 days. If they cannot verify the debt, it must be removed.

- Become an Authorized User

If you have a family member with a pristine credit history and a credit card with a high limit and low balance, ask if they will add you as an “authorized user.”

You do not need to possess or use the physical card. The entire history of that account (assuming the issuer reports authorized users) will be added to your credit file. This is often called “piggybacking” and can help establish credit history for first-time buyers or repair a score that has been damaged by high utilization.

- Handle Collections with Care

This is a tricky area. Many people think paying off an old collection account will instantly improve their score. Paradoxically, paying off an old collection can sometimes lower your score temporarily because it updates the “Date of Last Activity” to today, making the negative item look recent to the scoring algorithm.

Expert Advice: Before paying off old collections, consult with a mortgage professional like myself. We can run a “what-if” simulator to see if paying the collection will help or hurt your score. Sometimes, it is better to pay it at closing rather than beforehand.

Common Credit Pitfalls for Washington Residents

Living in Washington State presents specific scenarios that borrowers should be aware of.

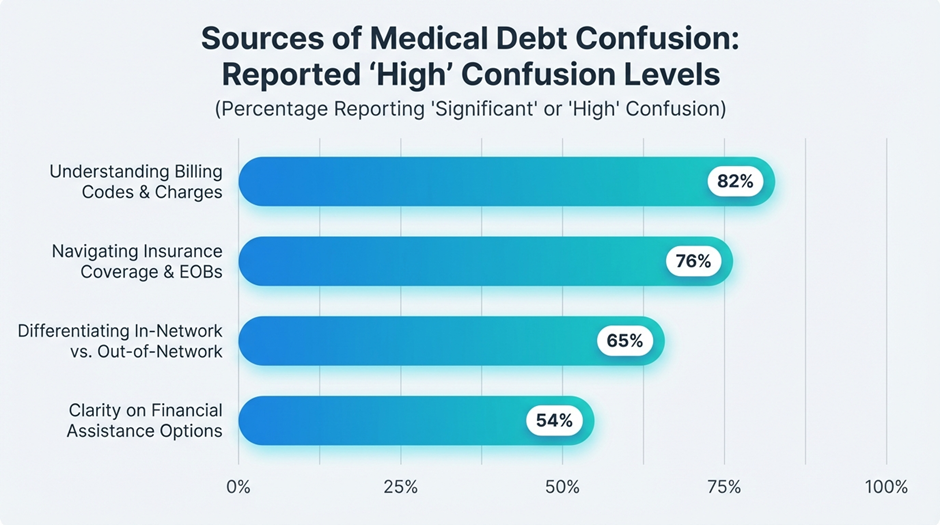

Medical Debt Confusion

Co-Signing for Family

In close-knit communities, it is common to co-sign for a child’s car loan or a sibling’s apartment. Remember: This debt is 100% yours in the eyes of a mortgage lender. If the primary borrower misses a payment, your credit crashes. Furthermore, that monthly payment counts against your Debt-to-Income (DTI) ratio, reducing the amount of home you can afford in Vancouver.

“Buy Now, Pay Later” Services

Services like Affirm, Klarna, or Afterpay are popular for online shopping. While they often advertise “no impact to credit score,” missed payments will be reported. Additionally, mortgage underwriters may view excessive use of these services as a sign of cash flow management issues.

The Cost of Waiting vs. Buying Now: A Comparison

Is it worth waiting six months to improve your score? Almost always, yes. The difference in interest rates between “Fair” and “Excellent” credit can amount to tens of thousands of dollars over the life of a loan.

Below is a hypothetical scenario for a home purchase in Vancouver, WA.

Scenario: $500,000 Loan Amount, 30-Year Fixed Mortgage.

| Credit Score Tier | Estimated Interest Rate* | Monthly Principal & Interest | Total Interest Paid (30 Years) | Cost of Low Score |

| 760+ (Excellent) | 6.0% | $2,997 | $579,190 | $0 (Baseline) |

| 700-719 (Good) | 6.25% | $3,078 | $608,245 | +$29,055 |

| 640-659 (Fair) | 7.0% | $3,326 | $697,543 | +$118,353 |

| 620-639 (Minimum) | 7.5% | $3,496 | $758,586 | +$179,396 |

*Note: Interest rates are for illustrative purposes only and fluctuate daily based on market conditions. This does not constitute a quote.

As you can see, improving your score from the 620s to the 700s could save you nearly $500 per month and over $100,000 in interest over the life of the loan. This is why we focus so heavily on credit strategy at Mortgage and Credit Pro.

How Mortgage and Credit Pro Can Help

I don’t just pull your credit and say “yes” or “no.” If your score isn’t where it needs to be, I work with you to create a customized plan. I have access to tools like Wayfinder and What-If Simulators that are not available to the general public. These tools allow us to see exactly which actions—paying down a specific card, transferring a balance, or removing an error—will yield the points needed to reach the next tier.

Whether you are a first-time homebuyer, a veteran looking to utilize a VA loan (which has great flexibility regarding credit), or looking to refinance, I am here to guide you every step of the way.

Ready to Check Your Eligibility?

You don’t have to guess. Begin my online application today to get a clear picture of where you stand. I pride myself on excellent communication and easy accessibility when you need me.

Frequently Asked Questions (FAQs)

- What is the minimum credit score required to buy a house in Vancouver, WA?

Generally, the minimum credit score for a Conventional loan is 620. However, FHA loans (backed by the Federal Housing Administration) allow for scores as low as 580 with a 3.5% down payment. For veterans, VA loans do not have a hard minimum set by the government, but most lenders look for a score of at least 580-620. Higher scores always result in better interest rates.

- How long does it take to repair my credit score for a mortgage?

It depends on the issues on your report. Paying down high credit card balances can boost your score in as little as 30 days (once the new balance reports to the bureaus). Disputing errors can take 30 to 45 days. However, recovering from major derogatory events like bankruptcy or foreclosure takes significantly longer. During our consultation, I can give you a realistic timeline based on your specific profile.

- Will checking my rate with you hurt my credit score?

When you formally apply for a mortgage, it results in a “hard inquiry,” which may temporarily lower your score by a few points (usually less than 5). However, the benefits of knowing your true standing far outweigh this minor dip. Furthermore, FICO models allow for “rate shopping”—multiple mortgage inquiries made within a 14-45 day window are typically treated as a single inquiry for scoring purposes.

- Can I buy a home if I have a bankruptcy in my past?

Yes, but there are waiting periods. For a Chapter 7 bankruptcy, you generally must wait 2 years from the discharge date for FHA/VA loans and 4 years for Conventional loans. For Chapter 13, you may be able to qualify sooner if you have made consistent payments on your repayment plan. We can review your discharge paperwork to determine your eligibility date.

- Should I pay off all my debts before applying for a mortgage?

Not necessarily. While less debt improves your Debt-to-Income (DTI) ratio, you also need cash for your down payment and closing costs. Depleting your savings to pay off zero-interest debt might leave you “house poor” or unable to cover closing costs. It is crucial to strategize with a mortgage professional to find the right balance between debt reduction and cash preservation.

Take the First Step Toward Your New Home

Don’t let credit uncertainty keep you renting in Vancouver. With the right guidance, homeownership is within reach. I am committed to helping you reach your goals with tailored loan solutions and expert advice.

Contact John Werner – Mortgage and Credit Pro

Phone: 1-623-363-0724

Email: john@mortgageandcreditpro.com

Related Posts