What if paying off your mortgage faster didn’t require a huge raise, winning the lottery,…

Your 2026 Homeownership Roadmap: Smart Strategies for Buying, Refinancing, and Building Wealth

As we look toward 2026, the real estate landscape continues to evolve. Whether you are a first-time homebuyer in Vancouver, WA, a current homeowner looking to leverage your equity in Oregon, or an investor scouting opportunities in Arizona, having a strategic plan is non-negotiable. Real estate remains one of the most consistent vehicles for building generational wealth, but the rules of engagement change with the market.

At Mortgage and Credit Pro, my goal is to simplify the complex. You have likely heard the horror stories: the mounds of paperwork, the strict qualification hurdles, and the anxiety of waiting for a closing date. My mission is to solve that for you. By offering tailored loan solutions and transparent communication, I help clients navigate the mortgage process with confidence.

This guide serves as your comprehensive roadmap for 2026, covering smart buying strategies, refinancing opportunities, and how to use mortgage tools to secure your financial future.

-

Assessing Your Financial Health: The Pre-Approval Foundation

Before you start scrolling through listings or planning a renovation, you need a clear picture of your financial standing. In 2026, lenders are looking for stability and reliability. Here is how to prepare your profile for the best possible interest rates and loan terms.

Understand Your Credit Profile

Your credit score is more than just a number; it is the gatekeeper to your interest rate. While many online tools offer a “consumer” credit score, mortgage lenders use a specific FICO model that weighs your history differently.

- Excellent (740+): Unlocks the most competitive rates for Conventional and Jumbo loans.

- Good (700-739): Solid options available, though rate adjustments may apply.

- Average/Fair (600-699): You are still in the game! FHA loans and VA loans are excellent vehicles for borrowers in this range.

If your score isn’t where you want it to be, do not panic. As a “Mortgage and Credit Pro,” I can review your report and offer guidance on how to optimize your score before you apply.

Debt-to-Income (DTI) Ratio

Lenders want to ensure you can afford your new mortgage payment on top of your existing obligations. Your DTI is calculated by dividing your total monthly debt payments by your gross monthly income. Keeping this ratio below 43% is a good target, though some loan programs allow for higher ratios with compensating factors.

Pro Tip: Avoid taking out new car loans or opening new credit cards 3 to 6 months before applying for a mortgage. Stability is key.

-

Strategic Buying in Vancouver, WA and Beyond

Whether you are looking in Vancouver, WA, Portland, OR, or Litchfield Park, AZ, the strategy for 2026 remains the same: match the loan product to your long-term goals. One size does not fit all.

First-Time Homebuyers: Breaking into the Market

If you are buying your first home, the down payment is often the biggest hurdle. However, it is a myth that you need 20% down. In fact, many of my clients get into homes with much less.

- FHA Loans: These are fantastic for buyers with lower credit scores or smaller down payments (as low as 3.5%). They offer flexibility that Conventional loans sometimes cannot.

- Conventional Loans: For those with stronger credit, you can purchase with as little as 3% down. These loans often have lower mortgage insurance costs.

The Power of VA Loans for Military Families

If you or your spouse have served in the US military (Army, Marine Corps, Navy, Air Force, Coast Guard, or National Guard), you have access to one of the best wealth-building tools available: the VA Loan.

Why VA Loans Win in 2026:

- $0 Down Payment: Keep your cash in savings or use it for renovations.

- No Mortgage Insurance (PMI): This saves you hundreds of dollars every month compared to other loan types.

- Flexible Credit Requirements: The VA program is designed to make homeownership accessible to those who served.

I specialize in helping veterans maximize their benefits. If you are unsure of your eligibility, contact me today so we can pull your Certificate of Eligibility (COE).

-

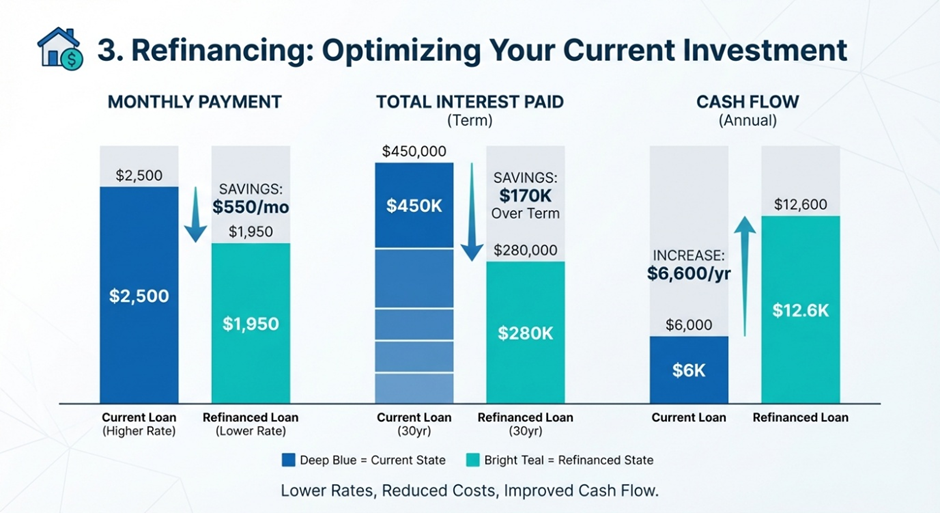

Refinancing: Optimizing Your Current Investment

Cash-Out Refinance: Tapping into Equity

Home values in the Pacific Northwest and Arizona have seen significant appreciation over the last few years. A cash-out refinance allows you to replace your current mortgage with a new one for a higher amount, giving you the difference in cash.

Smart uses for Cash-Out Equity:

- Debt Consolidation: Pay off high-interest credit cards or personal loans. Rolling these into a tax-deductible mortgage interest rate can save families hundreds, sometimes thousands, per month.

- Home Improvements: Reinvest in your property to increase its value further. Kitchen remodels and ADU (Accessory Dwelling Unit) additions are popular in Vancouver, WA.

- Investment Capital: Use the cash as a down payment on a second property.

Rate and Term Refinance

-

Building Wealth Through Real Estate Investment

Moving from a homeowner to a real estate investor is a major milestone in your financial roadmap. Whether you are looking at a multi-family property in Washington or a vacation rental in Arizona, investment property loans are different from primary residence loans.

Key Considerations for Investors:

- Rental Income: We can often use projected rental income to help you qualify for the loan (DSCR loans or standard investment loans).

- Larger Down Payments: Investment properties typically require 20-25% down to secure the best rates.

- Reserves: Lenders will want to see that you have cash reserves to cover vacancies or repairs.

Comparing Loan Options: Which Fits Your 2026 Goals?

| Loan Type | Ideal For | Min. Down Payment | Credit Flexibility |

| Conventional | Strong credit borrowers, Investment properties | 3% – 5% | Strict |

| FHA | First-time buyers, Lower credit scores | 3.5% | Flexible |

| VA Loan | Veterans & Active Military | 0% | Very Flexible |

| Jumbo | Luxury homes exceeding loan limits | 10% – 20% | Strict |

Why Choose a Local Broker Over a Big Bank?

In a competitive market like Vancouver, WA, who you work with matters. Big banks often operate on “banker’s hours” and treat applications like numbers in a queue. As a local Mortgage Broker, I operate differently.

The Broker Advantage:

- Choice: I am not tied to one bank’s products. I shop multiple lenders to find the specific rate and program that fits your scenario.

- Speed: In real estate, delays kill deals. I pride myself on excellent communication and accessibility. You can text me, call me, and count on me to move fast.

- Local Knowledge: I understand the nuances of the Oregon, Washington, and Arizona markets. I know what local appraisers look for and how to structure offers that sellers accept.

Frequently Asked Questions (FAQs)

- How do I know if I am ready to buy a home in 2026?

You are likely ready if you have a stable income, a manageable debt-to-income ratio, and some savings for a down payment and closing costs. However, you don’t need to be “perfect.” Getting pre-approved is the best way to find out exactly where you stand and what price range you can afford.

- What is the difference between Pre-Qualification and Pre-Approval?

Pre-qualification is an estimate based on self-reported data. Pre-approval is a verified commitment from a lender based on your actual financial documents (W2s, bank statements). In 2026, sellers will expect a Pre-Approval letter to take your offer seriously.

- Can I buy a home if I am self-employed?

Absolutely. While big banks can be tough on self-employed borrowers, I have access to loan programs specifically designed for business owners, 1099 contractors, and freelancers. We may look at bank statements rather than just tax returns to calculate your income.

- Is it better to refinance now or wait?

This depends on your goal. If you need cash out for high-interest debt consolidation, waiting might cost you more in monthly interest payments on credit cards than refinancing now would. If you are looking for a pure rate drop, we can analyze the break-even point to see if the savings justify the closing costs.

- How much are closing costs usually?

Closing costs typically range from 2% to 5% of the loan amount. This includes appraisal fees, title insurance, and recording fees. In some cases, we can negotiate for the seller to pay a portion of these costs, or structure the loan to minimize your out-of-pocket expense.

Let’s Build Your Roadmap Together

Whether you are looking to buy your first home in Vancouver, refinance in Portland, or invest in Arizona, you need a partner who is committed to your success. I am here to guide you every step of the way, from application to closing.

Don’t leave your financial future to chance. Let’s create a strategy that builds wealth and secures your homeownership dreams for 2026.

Ready to get started?

Related Posts